An assessment of the construction industry…

The Creditsafe Quarterly “Watchdog” report makes interesting reading for Q2 2018. Construction is reported to have bounced back in Q2 after the bad weather of Q1 caused delays and a drop in output. In April, May and June this year, the performance of the sector was mixed. Despite the increase in sales, 888 construction businesses went bust during these three months and the trend of falling profits continued amongst companies filing their latest accounts during this quarter.

From the perspective of credit insurance the figures are not rosy; in Q2, businesses in the sector were hit with a total of £9,569,111 of bad debt. The average amount of each bad debt was £14,744. The 888 construction companies which failed left behind £50,210,558 of debt owed to other companies, an average of £10,304 per creditor.

There’s an interesting table included in the Creditsafe report – the Top 5 “Most Searched” companies in the sector during the last quarter. Interserve is the number 1 most searched – no surprise there given the news around them. Kier is listed as the second most searched company, having been searched 1,247 times by Creditsafe subscribers. If searches are seen as reflective of concerns about a business then Kier’s listing at number 2 might be interpreted as reflecting concerns amongst its supplier base? Number 5 on the list was Ikon Construction; Ikon went into administration in May leaving £9.85m creditors. Creditsafe is not the only one to issue a report for the construction sector.

Bibby Financial Services has also released a paper entitled ‘Subcontracting Growth 2018’ taking a look back at the impact of major insolvencies in the sector. They report that the failure of Carillion in January affected more than 30,000 businesses in its supply chain and that insolvencies were up 73% in the first quarter as a direct result.Working with Vinden Partnership, Bibby surveyed 250 subcontractors to look at the state of the industry. Key findings include:

• 53% of businesses in the sector have written off money as bad debt in the last 12 months

• The average value of each write off was £16,000

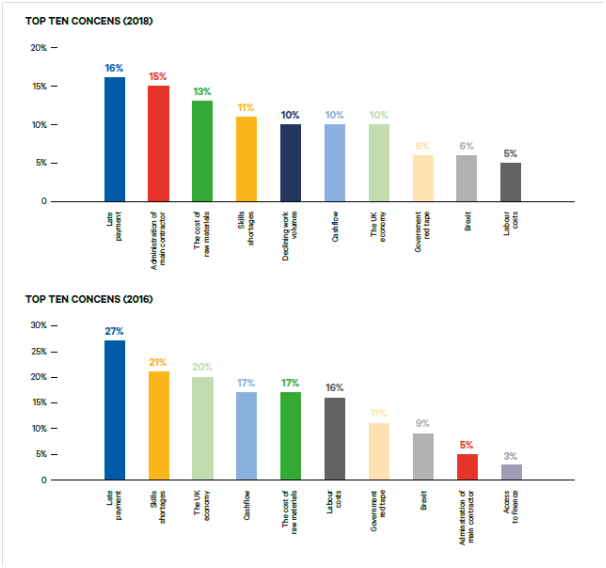

• Late payment is considered the primary concern for the business

The survey quantified that businesses are expecting a 30% uplift in cost of materials following Brexit, and that businesses would support the introduction of mandatory payment terms to stabilise future cashflow.Interestingly, the report has identified a shift in the concerns of businesses following recent industry changes, with ‘skills shortage’ slipping from second to fourth place in the last two years, the cost of raw materials jumping from fifth to third place and the introduction of a new concern – the administration of the main contractor – popping up in second place.

Perhaps of key concern from the perspective of managing risk are the reasons for bad debt. 79% of subcontractors do not always receive the amount that they bill for, writing off money as bad debt. The top three reasons for non-payment are: customer going out of business project brief changed partway through queries over quality of work.Whilst The Channel Partnership provide insurance against the first of these, the second two “contractual disputes” remain part of the routine cut and thrust of construction.